Committees approve financing bill

7 diciembre 2018

On December 5, members of the Senate and House of Representatives Finance and Budget Committees passed the Financing Bill. During the session, legislators introduced modifications to the bill, but none of pertinence to the sector. The bill will be debated in both chambers. Congress intends for the proposal to be approved in December.

Main features of the bill:

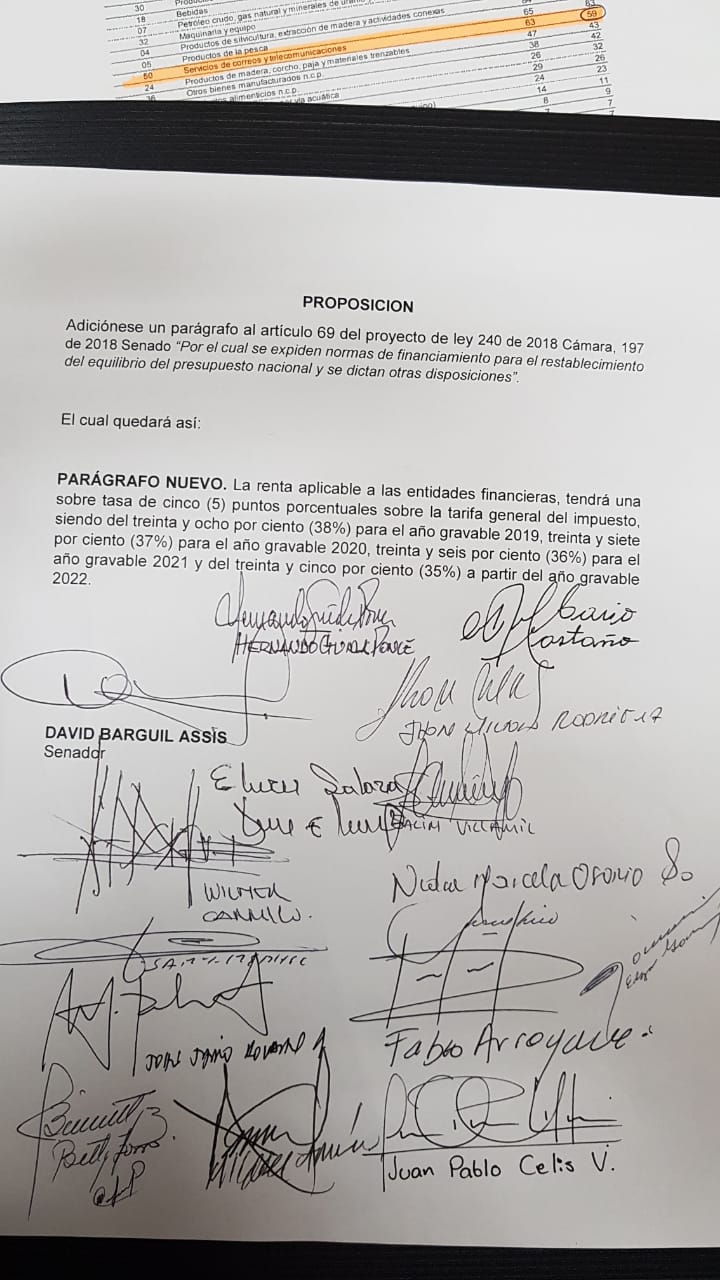

- The bill maintains a gradual reduction in income tax for businesses from the current 33% to 32% in 2020, 31% in 2021 and 30% from 2022. For lack of government support, the bill does not contain the proposal by Senator David Barguil (Partido Conservador-ally of the ruling party) to impose a 5% income tax surcharge on the financial sector. Barguil has stated he will seek to reintroduce the proposal on the chambers’ floors.

- The VAT rate will stay at the current 19%. A gradual reduction in this tax as well as its application to the household basket have been ruled out.

- A new tax on financial services and foreign exchange transactions is introduced. In financial services, the tax will be determined by applying the tariff to the taxable base. This base will be integrated in each operation, for the total value of the commissions and other remunerations received by the person responsible for the services rendered, regardless of their denomination. In exchange operations, the tax shall be determined by the intermediaries of the exchange market and by those who buy and sell.

- Presumptive income will be gradually eliminated from the current 3.5% to 2.5% in 2019, to 1.5% in 2020 and then 0% as of 2021. Previously, the bill stipulated a tariff of 3% by 2019.

- The income tax rate for dividends received by foreign companies with no principal office of business in the country increases from 5% to 7.5%.

- A 50% discount (2019-2020) and a 100% discount (from 2022) is stipulated against income tax for the Industry and Commerce Tax (ICA) which will become effective when paying income tax. The ICA depends on the local governments and, in the case of commercial activities and services, stipulates a monthly levy of between 0.2 and 0.10% to the monthly average gross income obtained in the previous year.

- Instead of a 50% discount against income tax, there will be a 50% deduction on the Financial Movement Tax (GMF), regardless of whether it is causally related to the income-generating activity. The GMF establishes a tariff of approximately US$ 0.0014 for each US$ 0.35 spent in any transaction.

{kind=link}

- The bill paves the way, as of January 1 2019, for a unified tax system under the new SIMPLE regime. It will be an optional taxation model that will replace income and complementary taxes, consumption taxes, industry and commerce taxes, in order to streamline the tax system and encourage the generation of employment. SIMPLE will be optional for natural and legal persons, but foreign legal persons (or their permanent establishments), entities that are affiliates, subsidiaries, agencies, branches of national or foreign juridical persons and companies that are not financial entities, among others, will be excluded.

- The initiative stipulates that for SIMPLE taxpayers, revenues resulting from sales of goods or services made through credit and/or debit card systems and other electronic payment mechanisms will generate a tax credit (or discount) equivalent to 0.5% of the income received through this means, according to certification issued by the acquiring financial institution. However, this discount may not exceed the total tax burden payable by the SIMPLE taxpayer.

- The initiative proposes that credit and debit card issuers will have to withhold payment for all services provided through digital platforms as well as the provision of rights of use or exploitation of intangibles and other electronic or digital services to users located in Colombia. Currently, they must only do so for the provision of audiovisual services (including, but not limited to, music, videos, films and games of any kind, as well as the broadcasting of any type of event), the digital distribution platform service for mobile applications, the provision of online advertising services, and the provision of distance learning or training.

- Goods subject to postal traffic worth USD 200 or less will be exempted from tax. At present, only the importation of goods subject to urgent shipments or quick delivery shipments with a value equal to or less than USD 200 are tax-exempt.